Oil Spikes, Mining Slides, and Market Signals This Month

Market Dynamics in March: Oil Volatility, Metals, and Sentiment Shifts

March has been a month of significant movement in global markets, with oil prices driving much of the action. The energy sector has experienced sharp fluctuations, which have had a ripple effect across commodities and equity markets. Alongside this, there are early signs of shifting sentiment that investors should be aware of as they navigate the current economic landscape.

Key Themes in the Energy Sector

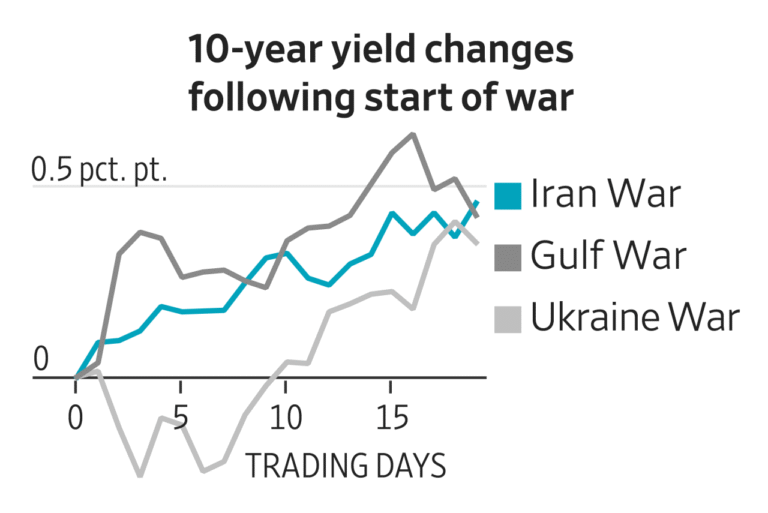

Oil prices have seen dramatic swings, largely influenced by geopolitical events, particularly those involving Iran. These movements have not only affected the commodity itself but also impacted energy stocks. According to Bruce Campbell of Stonecastle Investment Management, oil has made a four standard deviation move above the 50-day moving average — an event that is rare in historical context. While the commodity tends to spike and then settle back down, energy stocks often behave differently. Even when oil prices fall, energy stocks have historically shown positive returns over various time horizons.

This suggests that energy stocks may be responding to factors beyond just the price of oil, such as investor sentiment and broader market conditions. For value investors, volatility can present opportunities, while more conservative or short-term investors need to be cautious about entry points. Long-term investors, on the other hand, can benefit from absorbing some short-term fluctuations.

Metals Markets: Stability Amid Equity Pullbacks

In the metals sector, both precious and base metals have remained relatively stable in terms of underlying prices. However, mining equities have pulled back, creating a disconnect between commodity performance and stock valuations. This divergence can be attributed to several factors, including uncertainty in the market and rising production costs driven by higher oil prices.

Gold has maintained its stability, while silver has shown more volatility, fluctuating between approximately $75 and $95. Despite these price ranges, many mining stocks have declined by 10 to 15 percent or more from their peaks. This is a normal reaction to market uncertainty and increased operational costs.

Emerging Opportunities in the Resource Sector

Despite the challenges, there are still opportunities emerging in the resource sector. Bruce Campbell highlights that even if commodity prices remain within a tight range, certain projects could become profitable that weren’t before. Additionally, increased mergers and acquisitions (M&A) activity is expected as larger companies look to acquire projects rather than develop them from scratch.

Macro Indicators and Investor Sentiment

From a top-down perspective, several warning signals are beginning to emerge. Macroeconomic indicators, investor positioning, and sector breadth all point toward a more selective investment environment. This shift in sentiment suggests that investors should approach the market with caution, especially in the U.S. large-cap markets like the S&P 500 and Nasdaq.

Bruce Campbell notes that capital flows are starting to change, with less money entering the market. This can lead to increased volatility, and as a result, portfolios are being adjusted to a more defensive stance. Monitoring these indicators closely will be essential for making informed decisions.

Seasonality and Market Patterns

Seasonality plays a crucial role in market behavior. Historically, markets tend to be strongest from fall through spring, roughly between October and May or June. Within this period, there are shorter cycles, such as a strong January followed by a lull in mid-February to mid-March, and then strength again into late spring.

As we enter this stronger period, the recent volatility aligns with what is expected seasonally. However, it’s important to remember that seasonality sets expectations rather than guarantees outcomes. Short-term conditions can still vary, so investors should remain vigilant.

Geopolitical Considerations and Future Outlook

Geopolitical developments, particularly those involving Iran, will continue to influence markets. Additionally, the renegotiation of the U.S., Mexico, and Canada trade agreement could introduce new sources of volatility. As these factors unfold, investors should stay informed and monitor dashboard indicators closely.

Looking ahead, a defensive approach may be necessary as we head into the seasonally weaker summer period. By staying attuned to these dynamics, investors can better position themselves for potential opportunities and manage risks effectively.