S&P 500 Death Cross Emerges Amid US-Iran Tensions Before NFP Release

The S&P 500 Index has experienced a significant decline over the past week, continuing a downward trend that has been influenced by ongoing tensions in the Middle East. The conflict involving Iran has escalated, leading to increased prices for crude oil and natural gas. This situation has contributed to a broader sense of uncertainty in financial markets.

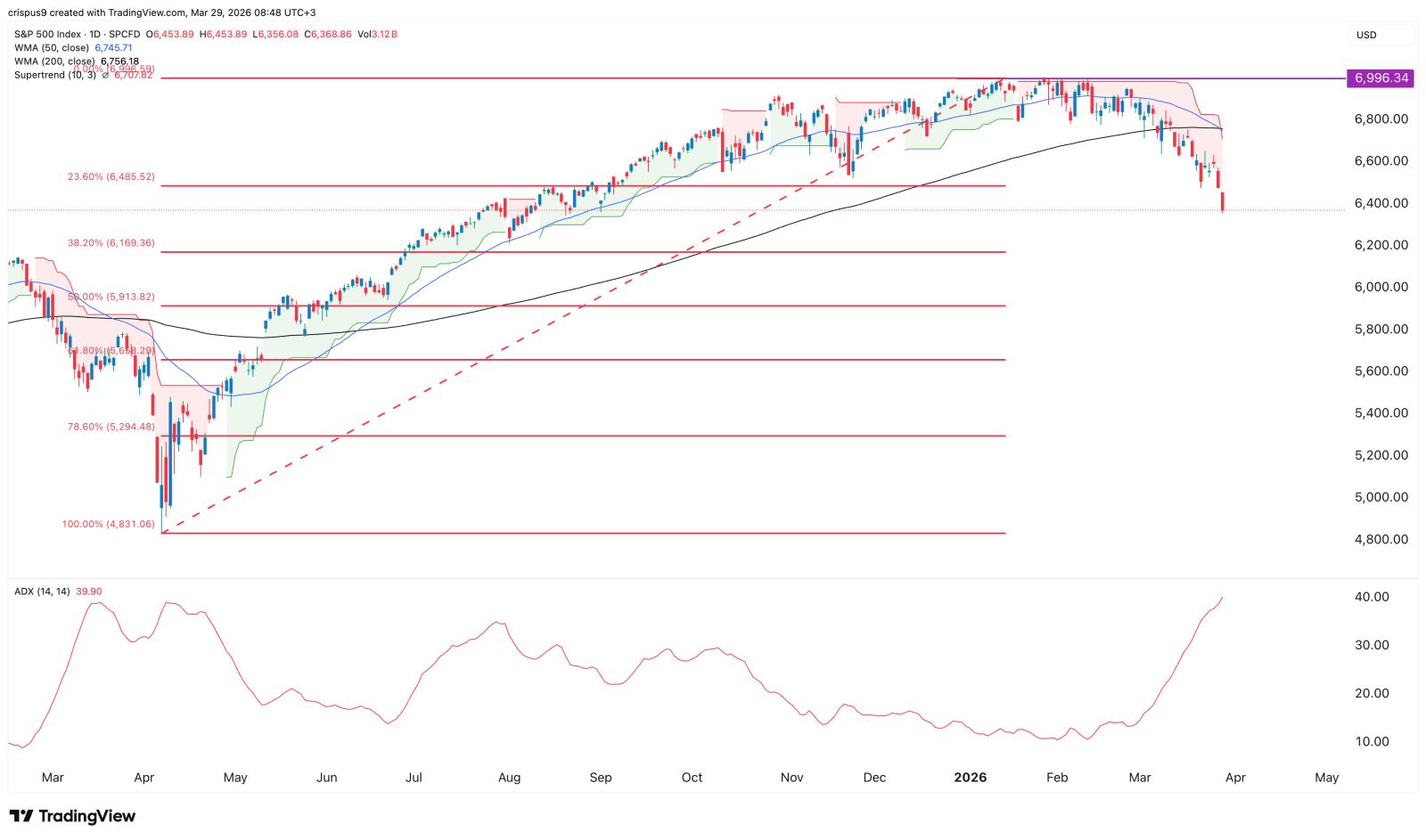

The SPX index reached $6,368, marking its lowest point since August of the previous year. This is the fifth consecutive week of declines, indicating a persistent bearish sentiment among investors. As the situation between the United States and Iran evolves, the S&P 500 Index and other major American indices, such as the Dow Jones and the Nasdaq 100, are expected to remain under close scrutiny.

Recent developments have added new layers of complexity to the regional conflict. Yemen’s Ansah Allah, commonly referred to as the Houthis, has entered the fray by launching rockets toward Israel. This group has pledged to continue its military actions in the coming weeks, which could pose challenges for oil tankers navigating through the Red Sea. In response, the United States has deployed additional troops to the region, with strategic objectives focused on securing control of Kharg Island and the Strait of Hormuz.

These events suggest that the conflict will persist in the near future, likely driving energy prices higher in the coming weeks. Data from recent weeks indicates that Brent crude and West Texas Intermediate (WTI) have surged to $112 and $100 respectively, representing an increase of over 100% from their annual lows. A prolonged conflict is expected to further depress the S&P 500 Index.

Another key factor influencing the S&P 500 Index is the upcoming release of US non-farm payrolls (NFP) data, scheduled for this Friday. Economists anticipate that the labor market may show signs of recovery in February after experiencing job losses in the prior month. The average forecast suggests that the economy could add 60,000 jobs in March, following a loss of 92,000 jobs in the previous month. The unemployment rate is expected to rise slightly from 4.4% to 4.5%.

Despite these expectations, the labor market has shown limited growth over the past few months. This trend may continue as the ongoing conflict in Iran impacts economic stability. The anticipated job gains are partly attributed to healthcare sector hiring, including over 30,000 Kaiser Permanente employees who ended their strike.

A weaker jobs report could be positive for the stock market, as it might pressure the Federal Reserve to consider interest rate cuts. However, the current economic environment is marked by stagflation, characterized by high inflation and sluggish economic growth. This complicates the Fed’s decision-making process.

In addition to labor market data, the S&P 500 Index will also respond to the upcoming manufacturing and services Purchasing Managers’ Index (PMI) reports from the United States. Economists expect these indicators to show a modest decline in March, driven by rising energy prices due to the ongoing conflict.

S&P 500 index Index chart | Source: TradingView

On the technical analysis front, the S&P 500 Index has shown a notable decline, moving from a peak of $7,000 in February to its current level of $6,368. The index has fallen below the 23.6% Fibonacci Retracement level. Additionally, the index has formed a death cross pattern, where the 50-day and 200-day Weighted Moving Averages (WMA) have crossed.

The Average Directional Index (ADX) has risen to 40, signaling that the downtrend is gaining strength. The index has also moved below the Supertrend indicator. These technical signals suggest that the S&P 500 Index is likely to continue its downward trajectory, with the next critical target being the 38.2% retracement level at $6,130.