Should You Invest in Defense Stocks After Record Gains?

The Growing Complexity of the Defense Sector

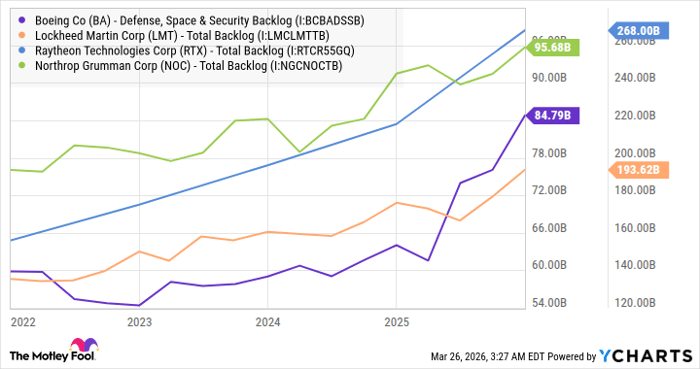

Backlogs and revenue expectations are on the rise as wars and geopolitical tensions continue to escalate. This has led the U.S. government to increasingly leverage its negotiating power to push defense companies to meet their contractual obligations. However, despite these growing backlogs, defense companies have found it challenging to maintain profit growth above a low-single-digit annual rate over the past decade.

Investing in defense stocks during times of intense geopolitical conflict may seem like a straightforward choice, but it is not without its complexities. While backlogs and revenue are increasing, and there is considerable upside potential, investors must also consider valuations and profitability. Recent developments, such as framework agreements between the U.S. government and major players like Lockheed Martin, BAE Systems, and Honeywell, highlight the ongoing efforts to accelerate production of critical missile technology. Yet, these factors alone do not guarantee success.

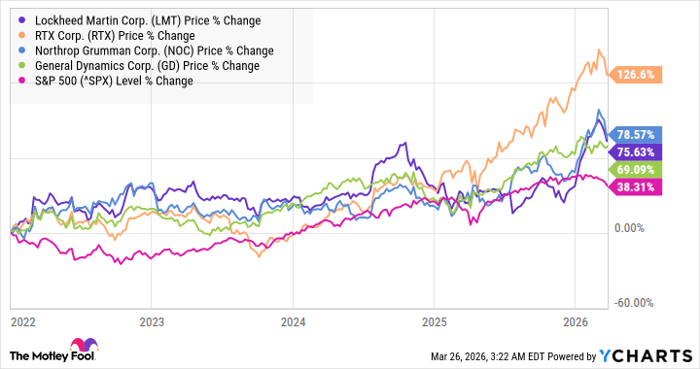

Soaring Tension, Soaring Share Prices

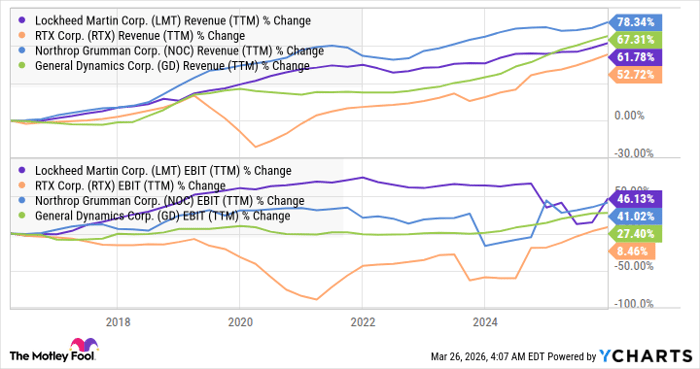

Defense stocks have outperformed the S&P 500 since Russia’s invasion of Ukraine in 2022.

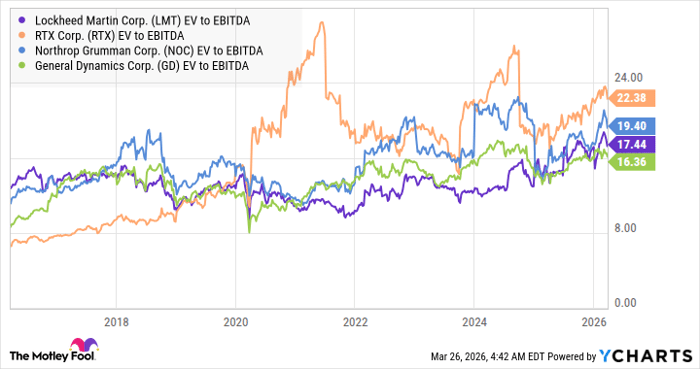

These backlogs have contributed to an increase in enterprise value—measured as market cap plus net debt—relative to earnings before interest, taxes, depreciation, and amortization (EBITDA).

Structural Margin Pressures?

A decade-long analysis of earnings before interest and taxes (EBIT) and EBIT margins reveals that declining margins have posed significant challenges for defense companies in growing profits. For instance, Lockheed Martin’s 46% increase in EBIT over the last decade translates to less than 3.9% annual growth.

The profit margin challenges appear to be structural and long-lasting, influenced by increasing technological complexity and heightened negotiating pressure from the U.S. government. This pressure is particularly evident in fixed-price development contracts and the demand for timely delivery.

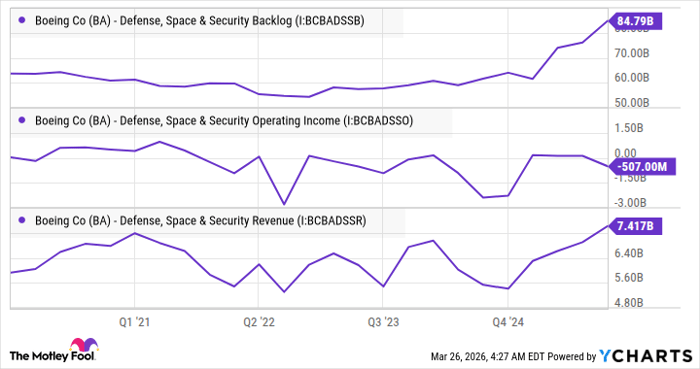

Boeing stands out in this context. Although fixed-price contracts account for only 15% of its defense segment’s revenue, they have resulted in multibillion-dollar losses and charges.

The Impact of Geopolitical Conflicts

The conflict with Iran has inevitably raised revenue expectations. However, if margin pressures prove to be structural and lasting, investors may be betting on new conflicts to drive revenue expectations and defense budgets even higher. This raises the question: Are current valuations justified for an industry that could struggle to grow earnings at more than a single-digit annual rate?

Caution may be necessary here, given the potential for prolonged margin pressures and the uncertain nature of geopolitical events.

A Second Chance at Potential Success

Ever felt like you missed the boat when investing in successful stocks? If so, now may be the time to reconsider. On rare occasions, expert analysts issue “Double Down” stock recommendations for companies they believe are about to experience significant growth. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late.

The numbers speak for themselves:

- Nvidia: If you invested $1,000 when we doubled down in 2009, you’d have $434,524!*

- Apple: If you invested $1,000 when we doubled down in 2008, you’d have $47,376!*

- Netflix: If you invested $1,000 when we doubled down in 2004, you’d have $503,861!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor. There may not be another chance like this anytime soon.

See the 3 stocks »

Stock Advisor returns as of March 29, 2026.