Unshocked by the Bull Market: Wall Street Focuses Beyond Iran Tensions

Market Volatility and Signs of Recovery

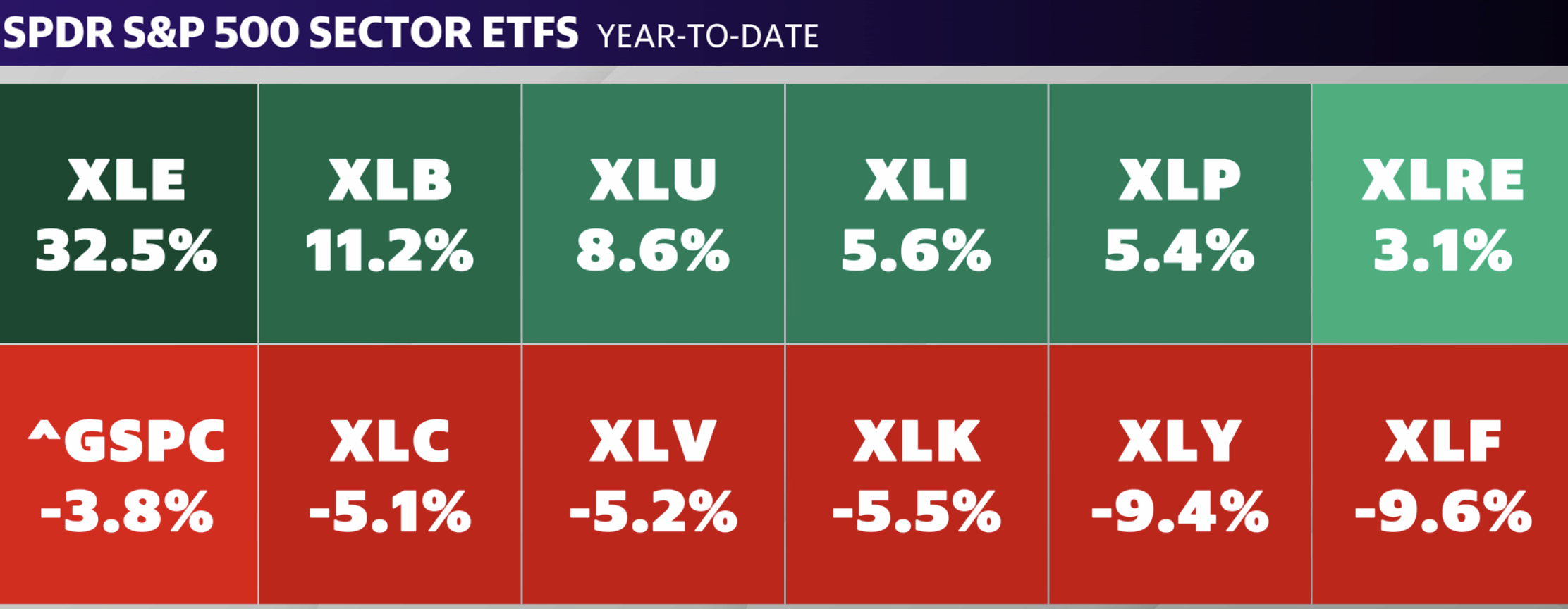

Despite recent fluctuations, Wall Street analysts are noticing signals that the market might be looking beyond the ongoing conflict in Iran. While oil prices have remained above $100 since the conflict began, the S&P 500 (^GSPC) has declined by approximately 4% and is nearly 6% below its all-time high.

Ryan Detrick, chief market strategist at Carson Group, shared his insights with Yahoo Finance, stating, “The message of the market is there’s still something in there.” He added, “We’ve withstood so much negativity, and everyone is so worried on the other side — that maybe that beachball under the water gets some good news and that ball can go up.”

A sign of this potential shift occurred last Tuesday when the S&P 500 surged by 2.9%, marking its largest gain since May. This was triggered by President Trump signaling a possible reduction in military presence in Iran over the next two to three weeks.

Ed Yardeni and Elias Griepentrog from Yardeni Research commented on this rebound, saying, “If Trump is declaring mission accomplished, then so are we regarding our stock market correction call.” They indicated that their firm may lower its recession probability from 35% to 20% once there is more clarity on whether the Middle East conflict has truly ended.

However, they maintained their 7,700 S&P 500 year-end target and their belief in the “Roaring 2020s” base case.

Investor Confidence and Economic Outlook

UBS strategists highlighted the sharp rebound following positive headlines, emphasizing how a resolution to the conflict or even the hope of one can quickly boost markets. Ulrike Hoffmann-Burchardi, chief investment officer Americas at UBS Global Wealth Management, stated, “We continue to believe global stock markets will end the year higher than they are today.”

While some economists warn that prolonged energy costs could increase the risk of stagflation, Wall Street has not yet significantly revised profit forecasts due to a lack of data. Kevin Gordon, head of macro research and strategy at the Schwab Center for Financial Research, noted, “Maybe it’s because analysts have been just sort of flying blind a little too much lately, but we haven’t seen earnings estimates moved down in a material way.”

He added, “That is sort of a reflection of, so far, the data not showing that the economy is struggling, at least right now.”

Earnings Outlook and Sector Performance

Heading into the earnings season, companies and analysts have shown more optimism than usual in their outlook for the first quarter, according to FactSet data. The S&P 500 is expected to report year-over-year earnings growth of 13.2%, compared to the estimated 12.8% calculated at the end of last year. This would mark the sixth consecutive quarter of double-digit annualized earnings growth for the index.

Detrick from Carson Group said, “The volatility is uncomfortable, the headlines are uncomfortable. But if we look back 6-12 months from now, I wouldn’t be shocked at all if this bull market continues.”

For this to happen, the technology sector would need to regain momentum. Last quarter, the sector faced several challenges, including rising yields that pressured lofty valuations, profit-taking, and the loss of its equity safe-haven appeal.

Despite the recent market rebound, major tech stocks such as Tesla (TSLA), Alphabet (GOOG, GOOGL), Amazon (AMZN), Meta (META), Microsoft (MSFT), Apple (AAPL), and Nvidia (NVDA) are all down year-to-date.

Eric Jackson, founder of EMJ Capital, remarked on Opening Bid, “Mag 7 has gotten its head clobbered, especially in the last quarter. And that’s unusual for them.” He added, “I do think these guys are due to catch a bid in Q2 and Q3.”

Strategic Sector Recommendations

Goldman Sachs analysts have adjusted their strategy, favoring defensive, heavy-asset, and commodity-linked sectors given the ongoing energy-driven shocks from the Middle East conflict and the threat of AI disruption.

Their sector views include a preference for (1) Financials, (2) heavy-asset sectors with lower technology obsolescence risk, and (3) commodity- and defense-linked sectors. Key overweights include Banks, Insurance, Energy, and Aerospace & Defense.

Meanwhile, key underweights include Automotive, REITs, and Food & Beverage, due to their sensitivity to high interest rates and rising oil costs.